📅 May 11 2026 | ✍️ LiveGoldSignal.com | ⏱️ 7 min read

Two structural developments published over the weekend are reshaping how institutional investors are thinking about gold allocation heading into the second half of 2026. First HSBC Global Research published a note upgrading its gold price forecast for Q3 and Q4 2026 to $5200 and $5800 respectively citing the acceleration of central bank reserve diversification and the structural underallocation of gold in Western institutional portfolios. Second the World Gold Council published a supplementary analysis to its Q1 2026 demand report showing that gold’s share of global foreign exchange reserves has now crossed 20 percent for the first time since 1983 driven by a combination of price appreciation and continued sovereign buying. These two non-war structural developments plus today’s April CPI at 8:30 AM ET frame the week’s key question: is gold at $4714 fairly valued in a world where central banks are structurally reallocating toward it and where inflation is still running above 3 percent despite ceasefire progress.

HSBC Upgrades Gold to $5200 and $5800: The Institutional Case

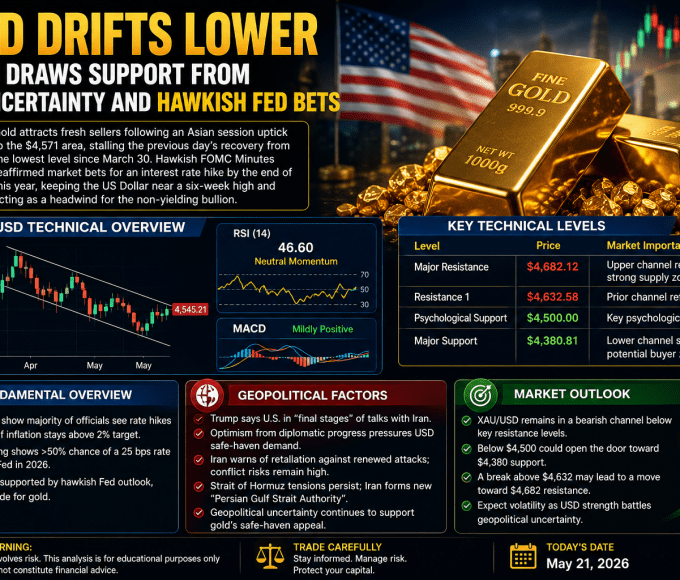

HSBC Global Research’s weekend forecast upgrade is significant for several reasons beyond the headline numbers. HSBC is one of the world’s largest physical gold market makers operating the London Good Delivery vaulting and trading infrastructure that underpins the global gold market. When HSBC publishes a gold price forecast it does so with access to physical market flow data that is not available to any research firm that does not participate directly in the bullion market. The bank’s upgrade to $5200 for Q3 2026 and $5800 for Q4 2026 reflects what its traders are seeing in actual client order flow: a significant increase in institutional buying of physical gold driven by asset allocators reweighting their portfolios toward real assets in response to the stagflation environment that Goolsbee officially confirmed last Thursday. The note specifically identifies three drivers for the upgraded targets. First ongoing central bank buying at a pace of approximately 244 tonnes per quarter will continue to provide a structural demand floor. Second Western institutional gold ETF allocations at 0.17 percent of total assets are rising as asset managers respond to client demand for inflation protection and the bank’s flow data shows the reallocation is accelerating in April and May. Third the oil price correction from $112 toward $95 to $101 following ceasefire progress is reducing inflation fears enough to allow rate cut probability to gradually recover which provides an additional medium-term tailwind for gold through the lower real yield channel.

The $5800 Q4 2026 target would represent a new all-time high exceeding the January 2026 record of $5595 by approximately 3.6 percent. HSBC analysts note that this target is based on their baseline scenario in which the Iran MOU formalizes into a full deal by June reducing oil prices to the $80 to $90 range which allows CPI to fall below 3.0 percent by August prompting the Federal Reserve to cut rates by 25 basis points at its September meeting. In this scenario all of gold’s near-term headwinds resolve simultaneously creating conditions for a sustained move to and beyond the prior ATH. The bank acknowledges a downside scenario of $4200 to $4400 if the MOU collapses and Iran conflict escalates driving oil back above $120 but rates this as a 20 percent probability versus the 80 percent probability assigned to the baseline recovery scenario.

Gold’s Reserve Share Crosses 20 Percent: A 43-Year Milestone

The World Gold Council’s supplementary analysis confirms that gold’s share of global foreign exchange reserves has crossed 20 percent for the first time since 1983. This milestone has been approaching since 2022 when the freeze of Russian foreign exchange reserves triggered a structural reassessment of reserve composition across dozens of central banks. The WGC notes that the 20 percent threshold is significant not just as a round number but as the level that historically has been associated with active reserve accumulation phases: when gold’s reserve share rises through 20 percent it tends to attract additional sovereign buying as reserve managers benchmark against global averages and seek to bring their own allocations in line with the emerging norm.

| Year | Gold Reserve Share | Key Context |

|---|---|---|

| 1960 | ~60 percent | Bretton Woods era gold-backed dollar system |

| 1971 | ~40 percent | Nixon closes gold window end of Bretton Woods |

| 1980 | ~25 percent | Peak post-Bretton Woods gold rally price $850 |

| 1983 | ~20 percent | Last time gold exceeded 20 percent share |

| 2000 | ~8 percent | Post-Cold War dollar dominance era low point |

| 2022 | ~13 percent | Russian asset freeze triggers diversification |

| 2025 | ~18 percent | Three consecutive years above 1000 tonnes annual buying |

| 2026 Q1 | ~20 percent | First crossing above 20 percent since 1983 |

The historical pattern in the table above reveals an important structural dynamic. Gold’s reserve share fell steadily from the 1980 peak as the dollar system strengthened and central banks treated gold as an anachronistic relic. The 2000 low of approximately 8 percent represented the maximum underweight position before the structural reversal began. Since 2000 gold’s reserve share has risen from 8 percent to 20 percent driven by a combination of price appreciation and sustained net buying. The 20 percent level represents the midpoint between the 2000 trough and the 1980 peak which suggests the structural reallocation has approximately the same distance to travel upward as it has already traveled from the 2000 low. If the historical pattern holds and gold’s reserve share eventually returns toward 25 to 30 percent the implied price appreciation from the current $4714 would be enormous given that total global FX reserves are significantly larger in dollar terms than they were in 1980.

April CPI Preview: What the Oil Price Retreat Means for Inflation

Today’s April CPI is the most anticipated data release of the week because it will be the first reading to show whether the oil price retreat from the $112 March peak is feeding through into lower consumer prices. The mechanics of oil’s CPI impact operate with a lag of approximately four to six weeks for gasoline and two to three months for broader energy and food components. Brent oil averaged approximately $105 to $112 in March. In April the average fell toward $98 to $105 as ceasefire negotiations progressed and the US and Iran both indicated willingness to engage on an MOU framework. If this price reduction has begun appearing in April gasoline prices the CPI energy component could show a meaningful month-on-month decline after March’s sharp increase. An energy CPI decline combined with a stabilizing core CPI (which excludes energy and food) would produce a headline CPI reading that shows the first meaningful deceleration from March’s 3.3 percent. Analysts at Goldman Sachs and Wells Fargo both publish pre-CPI notes projecting April headline at 3.0 to 3.1 percent with the energy component accounting for most of the expected decline from March’s level. If Goldman and Wells Fargo are correct a 3.0 to 3.1 percent CPI today would revive rate cut expectations and provide a direct additional catalyst for gold’s continued recovery toward $4759 and $4800 this week.

The Oil Price and Gold Connection: Understanding the Lag Effect

One of the most important but least understood dynamics in gold’s 2026 price action is the relationship between oil prices and gold through the inflation and rate expectations channel. Many investors assume falling oil is directly bearish for gold as a safe-haven asset. In reality the relationship is more nuanced and ultimately bullish for gold through the monetary policy channel. When oil falls from $112 to $95 to $101 as has occurred following ceasefire progress CPI falls within two to three months as energy costs feed through. Falling CPI reduces inflation fears. Reduced inflation fears allow the Federal Reserve to begin discussing rate cuts. Expected rate cuts lower real yields (nominal rates minus inflation expectations). Lower real yields reduce the opportunity cost of holding non-yielding gold. The net effect is that oil price declines following a geopolitical conflict are ultimately gold-positive through the monetary policy channel even as they remove the immediate war-premium component of the gold price. This is why gold has risen 4.2 percent from its correction low of $4510 even as oil has fallen from $112 toward $95 to $101. The removal of the war premium has been more than offset by the revival of rate cut expectations that falling oil enables. HSBC’s $5200 to $5800 year-end forecasts are built precisely on this dynamic: oil falling as the MOU matures allows CPI to fall below 3 percent by Q3 which enables the Fed to cut in September which sends gold to new all-time highs by year-end.

📌 News Summary May 11: HSBC upgrades gold forecast to $5200 Q3 2026 and $5800 Q4 2026. Drivers: central bank buying 244 tonnes per quarter Western ETF reallocation and rate cut revival from oil price retreat. WGC: gold reserve share crosses 20 percent first time since 1983. Historical milestone: from 8 percent in 2000 to 20 percent now same distance remains to 1980 peak of 25 to 30 percent. April CPI today consensus 3.0 to 3.1 percent. Oil retreat from $112 to $95 to $101 begins feeding into lower CPI with 4 to 6 week lag. Goldman and Wells Fargo: energy component declines produce first meaningful CPI deceleration. The structural case at $4714: HSBC $5800 WGC gold crossing 20 percent reserve share and Goldman $5400 all point to the same conclusion: gold is structurally undervalued at current levels relative to where sovereign reserve accumulation and institutional reallocation are taking it.

Risk Warning: Trading gold carries significant risk. Past performance is not indicative of future results. Educational purposes only. Not financial advice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}